Is It Time To Dump Traditional Monte Carlo Simulation Software For Retirement Spending?

By John H. Robinson, Financial Planner (February 2025)

Consumers who turn to financial planning professionals for retirement income planning guidance in the 2020s are usually presented with the Monte Carlo simulations as the tool for assessing their preparedness and plotting their spending plans. Within the financial planning community the simulations given to clients are often produced by applications from popular software makers such as eMoney, Money Guide Pro, Right Capital, and Income Lab. The output is often twenty or more pages long and replete with colorful charts and broomstick tables with results summarized as “probabilities of success”. Retail brokerage firms, such Schwab, Fidelity, and Vanguard have their own less sophisticated versions that they make available directly to consumers.

Recently, however, I have noticed a rising tide of resistance to the widespread use of traditional Monte Carlo simulation software from within the financial planning research community. At issue is whether the software produces sophisticated analysis or just the appearance of sophistication. Here is an illustrative example -

By conducting research assessing the performance of various Monte Carlo methodologies, Income Lab has suggested that, at a high level, Monte Carlo simulations experience significant error compared to real-world results. Additionally, certain types of Monte Carlo analyses were found to be more error-prone than others, including a Traditional Monte Carlo approach using a single set of Capital Markets Assumptions (CMAs) applied across the entire plan, and a Reduced-CMA Monte Carlo analysis, similar to the Traditional model but with CMAs reduced by 2%. [Source: How Different Monte Carlo Models Perform In The Real World: Assessing Quality Of Predictiveness In Retirement Income Forecasting Models, Kitces.com]

Problems with Monte Carlo Software

The most widely cited problem with the software, as referenced in the excerpt above, is that the results are dependent upon capital markets assumptions (CMAs) the user makes regarding the expected return and standard deviation for each asset class used in the simulation model. Since asset returns and volatility are not static over time, different applications use different asset mixes, and users make different assumptions, it is no surprise that a chief complaint with Monte Carlo software is that consumers get different results from different applications and even from different advisors using the same applications. This, of course, begs the question of which application’s projections is the most accurate?

Another criticism pertains to input complexity. While one might assume that software that incorporates the impact of taxes, integrates with estimated social security income, and optimizes account type spending order would be superior to simpler models, tax rates change fairly frequently and social security benefits, including cost of living adjustments, are are impossible to predict. Given that small errors lead to large value differences when illustrating longer periods of time, it is not wrong to suggest that input complexity is inversely correlated to output accuracy.

The Dangers of Monte Carlo Simulations (Advisor Perspectives)

A New Study Confirms: Conventional Financial Planning Is Worse Than We Think (Larry Kotlikoff, PhD.)

The Path Forward

The challenges listed above were recently described in two separate articles by respected academic researchers William Bernstein and Wade Pfau.

Here We Go Again: Merton Share and Why I Don’t Use Retirement Calculators (Bernstein, Advisor Perspectives)

Practical Considerations in Tax-Efficient Distribution Planning (Pfau, et. al, Advisor Perspectives)

“Tax-efficient withdrawal planning is not a set-and-forget service. How should advisors manage these plans through time? Communication between tax professionals and advisors is necessary to avoid missteps in implementation or tax reporting.”

The conclusion that both authors reach is that that financial planners should optimize their client’s spending each year, adjust account spending order in accordance with the existing tax regime and to adjust portfolio allocation and spending in accordance with the prior year’s investment environment.

How We Use Simulation Software

Financial Planning Hawaii and Fee-Only Planning Hawaii clients likely know that we eschew traditional Monte Carlo simulation software and that our own proprietary software, Nest Egg Guru, was created to address the problems referenced above. Instead of making return assumptions, Nest Egg Guru applies bootstrapped sampling techniques that produce simulation from random sampling of 50 years’ worth historical monthly return data for three equity classes (S&P 500 Index, Russell 2000 Index, and MSCI EAFE Index) and fixed returns for cash and bonds. This type simulation methodogy is sometime referenced as Historical Monte Carlo Models. Support for this structural difference is found in the following excerpt from the previously cited Income Lab research -

“Notably, Historical and Regime-Based Monte Carlo models outperformed Traditional and Reduced-CMA models not only in general, but also throughout most of the individual time periods tested, as they had less error across many types of economic and market conditions.”

Because all users use the same underlying sampling data, there is no variation in results across different users. Additionally, the Nest Egg Guru Retirement Spending App does not attempt to incorporate the impact of taxes and instead focuses on the gross distribution amount from the total retirement portfolio (i.e., it leaves it to the user to optimize account spending order as a separate exercise).

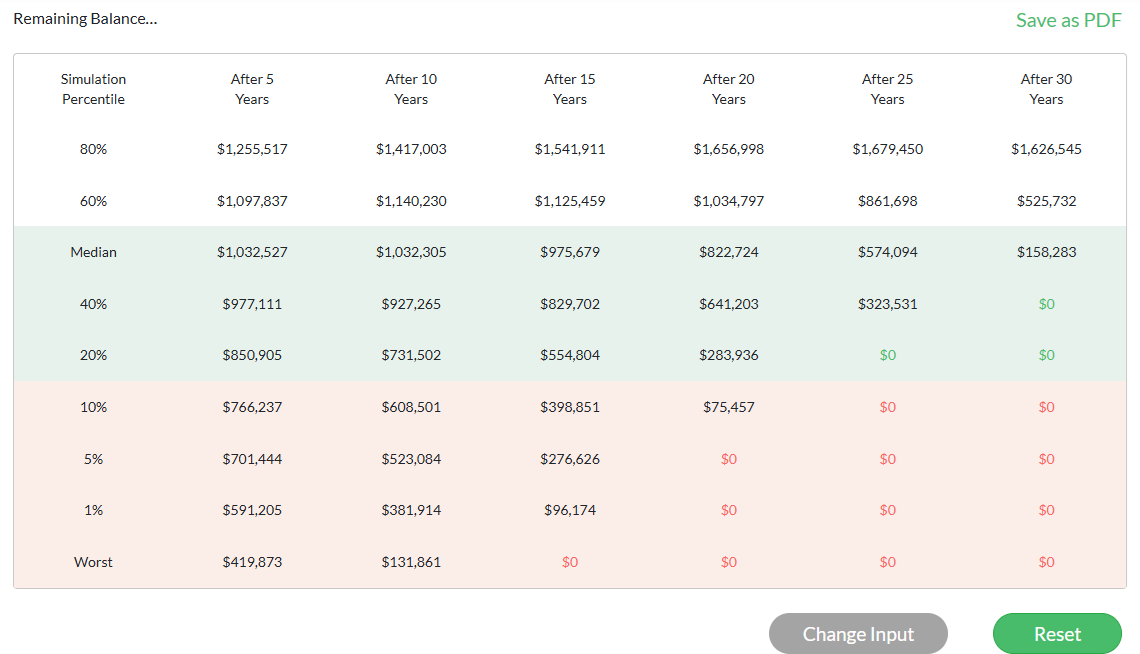

We believe Nest Egg Guru’s simulations are useful for providing an initial assessment of preparedness and for giving consumers a tangible sense of how their retirement portfolios may perform if future returns are average to modestly below average to historically awful (see sample output illustration below).

The software is also useful for quickly and easily educating users about the impact and efficacy of changing certain inputs that are within the consumer’s control, such as stock/bond allocations, cost of living adjustments, spending methodology (e.g., rebalancing, bonds-first, stocks-first, etc.). As you can see this illustrative/educational use-case for Nest Egg Guru’s simulation software is very different from predictive role of traditional CMA-based Monte Carlo software. In Nest Egg Guru, “probabilities of success” are nowhere to be found.

In conjunction with our educational use-case for Nest Egg Guru’s retirement spending software, I wholeheartedly agree with Drs. Bernstein and Pfau that consumers should not view the simulation results as the basis for a set-it-and-forget-in retirement spending plan. Instead, spending should be optimized each year with tax planning integrated with investment planning.

John H. Robinson is the owner/founder of Financial Planning Hawaii and Fee-Only Planning Hawaii. He is also a co-founder of fintech software maker Nest Egg Guru and the new personal finance website NestEggPF.com.